NOTE: May 2009 — For further updates on the oil price, see also:

The price of oil: 3 — energy economics and the financial crisis;

The price of oil: 4 – a rising road ahead.

It was a chilly evening in early February when the Managing Director called us all together. He paused a moment, glanced at the expectant faces all around him, and then he started.

It was a chilly evening in early February when the Managing Director called us all together. He paused a moment, glanced at the expectant faces all around him, and then he started.

Business is tough, he said, and we’re doing what we can. But finally, we’ve reached that moment when we’ve got to let some of you go.

A hundred of us stood there then, looking at each other, at the floor, and at the winter’s dusk outside.

There was silence. Some more explanation was required, and some more honesty was needed. And, to his credit, Mitch provided it. As ‘this company is going down the toilet’ talks go, it was pretty fairly done.

We’d had problems with one of our installations in the North Sea, he told us. We all knew that already. In the big money business of finding oil and gas and getting them to the beach, failing on either of those priorities was never good.

An asset team would miss its targets, and there’d be no bonuses or payrises for anyone ahead. Such is business, in any organisation. But this time, it was worse.

An asset team would miss its targets, and there’d be no bonuses or payrises for anyone ahead. Such is business, in any organisation. But this time, it was worse.

It’s the oil price, he said. February, 1999.

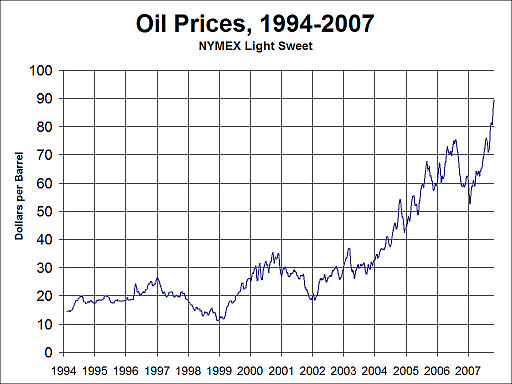

On that day nine years ago, the price of Brent Crude Oil from the North Sea stood at $9.80 a barrel, having fallen off a cliff to $9.20 in the December before.

Even then, it cost more than $12 a barrel to produce, and we were losing money on every barrel we delivered. It’s getting worse, he said, and we can’t see how it’s going to end. And no one could.

An analyst’s report in The Economist in the spring of 1999 said that with $10 oil a reality, there was nothing to stop a fall to $5. The market had changed, and changed for ever. There was a world glut of oil, with no resolution in sight.

Surely there are two sentences which should strike fear into the heart of any speculator, or anyone who has ever bought a house. ‘A structural change in the market’ – that’s one. And, ‘It’s different this time’ – that’s another.

It wasn’t then. But it is now.

It wasn’t then. But it is now.

In 1999, world oil production was at 75 million barrels of oil a day, and the Asian and Russian financial crises had removed enough demand, temporarily, to send the oil price plummeting.

Less than a decade later, the world is consuming 85 million barrels of oil a day, and produces almost exactly that much.

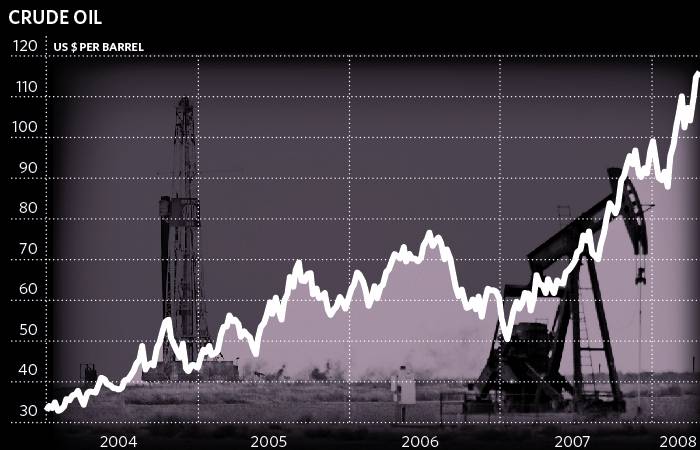

Within five years from that evening in 1999, the price of oil had more than tripled to $34 a barrel. It doubled again to $70 by the summer of 2005. And a few weeks ago, in January 2008, a barrel of Brent Crude Oil was trading at $98. In the space of just nine years, the price of oil had risen by exactly ten times.

In 1999, the North Sea was at its peak. UK oil production averaged 2.7 million barrels of oil per day that year. Further afield, Girassol, the first of a series of giant fields offshore Angola, had recently been discovered by Elf, and a string of new international successes followed. For a while.

By 2008, only nine years later, the UK’s production is down by almost half, at 1.4 million barrels of oil per day.

By 2008, only nine years later, the UK’s production is down by almost half, at 1.4 million barrels of oil per day.

This country is still a world-class oil and gas producer, and the North Sea will yield petroleum for another three decades to come. But not at the same rate. The basin has passed its peak, and production is declining by around 4% each year.

The North Sea is just one hydrocarbon basin amongst many all around the world. But they all follow the same trend. Every dog has its day, and every oil and gas province ever found is eventually drained. For as long as we don’t invest massively in alternative energy, then we’ll have to keep finding new reserves.

But what if we can’t? With highly memorable exceptions in 1973 and 1979, world petroleum supply has always risen to meet demand. Maybe not much longer, since production looks remarkably flat, these days.

In 2007, the Bush administration and Gordon Brown each called on the Middle East to boost production and stem the rise in oil prices.

But the OPEC states can’t manage that trick any more. Petroleum supply in 2006 was slightly lower than in 2005. Early data for 2007 suggest that supply was static, or falling slightly further still.

So here’s the paradox. We’re not running out of oil – and we won’t, for years to come. But right now we can’t pump oil and gas faster to meet new growth in world demand. Oil and gas production is virtually at its peak.

That’s why it really is different this time.

It was in December that I bought petrol at over £1 a litre for the first time (that’s $7.60 a US gallon, by the way). That might seem a high price to pay, until you realise that the UK’s petrol costs just about the same as milk. That’s remarkable, when you consider the technology and effort required to bring it to the pumps.

Petrol costs in Europe are largely sheltered from escalating oil prices because taxes on fuel are so high. Until recently, we’ve also been protected by the falling dollar. But prices are still rising – and petrol is at 104.9p a litre in London as I write today.

Petrol costs in Europe are largely sheltered from escalating oil prices because taxes on fuel are so high. Until recently, we’ve also been protected by the falling dollar. But prices are still rising – and petrol is at 104.9p a litre in London as I write today.

The North American consumer is not so protected. I can remember the outcry when gasoline first rose to $1 a gallon. And then $2, and $3 at one time, too. But that’s just the start – and even a recession in North America may not make much difference now. Because what will a recession do? A drop in GDP of 1 or 2%, for a year or two, with a slow recovery to follow?

That’s just not going to cut it. Even if the phenomenal economic growth in India and China grinds to a total standstill, which seems unlikely, then static world demand can’t change the fundamentals of depletion. The North Sea shows that the decline from peak production in any basin can be swift – by 4% a year, remember, or as much as 50% within a decade.

With so many hydrocarbon-producing basins around the world, we can hope that the decline will be more gentle than that, when it comes. But make no mistake, a decline is coming, and it’s not that far away.

In January 2008, the oil price touched $100. It’s slipped to $87 today. That’s not surprising, since the value of any commodity is always subject to the direction of the market – that weight of speculation which can add or subtract 30% from the fundamentals, at any given time. The oil price may fall further in the next few months – perhaps to as low as $60, or a little less.

But let’s not get too excited about $60 – that’s just the level of twelve months ago. Prices will rise again, eventually, and we won’t have long to wait – since the economics of falling supply and rising demand make that a rising certainty.

Let’s be clear. This isn’t about $100 oil. In the near future you can add another 50%, or even double that figure, and just keep on going.

What’s the world going to look like with oil at $200, $300, $400 a barrel ? That’s a crazy notion – it sounds like madness. And if you think so, then just go back and read this post again.

So, let me reiterate. The price of oil has risen 900% within the last nine years. It rose 50%, year-on-year inside the last twelve months to reach that $100 peak. Maybe not tomorrow, but before too long, you can double that again. And after that, you can just keep on going.

This world of ours is going to look very different, very soon. Peak oil is happening, and it’s happening today.

: :

: :  : :

: :  : :

: :  : :

: :  : :

: :

Related articles:

105. A crisis of energy

110. The hands that built America – Houston skylines

69. Running low on fuel

133. Tomorrow – Avril Lavigne and global warming

UPDATE 30.04.2008

When this article appeared in February 2008, the oil price stood at $87, down from $100 in January. Less than three months later, the oil price is hovering close to $120. The graph below from The Independent illustrates that rise.

Today’s oil price is at around 400% of the January 2004 level, and close to 250% of the figure for January 2007. Will the curve level off, or will it continue to extrapolate upwards? That’s the subject for a fascinating debate.

And corporate America cashes in – Exxon beat its own record last year for highest profit ever recorded by a U.S. company: http://www.iht.com/articles/2008/02/01/business/exxon.php

Thanks, Elayne – that’s a good point, and the same applies in Europe, too. Shell sets new UK record profits

But these reports hide a different problem. The majors are seeing rising cashflow, but they are failing to meet their targets for production growth.

The fundamentals are essentially the same for oil-producing nations as for major oil companies. None of them is capable of increasing production.

The reasons for this are open to debate – in part this may reflect low investment levels resulting from excessive caution after the oil price crash of 1986 and the 1999 event I cite above.

But the increasingly likely, alternative possibility is that there just may not be enough hydrocarbons left to bring on stream tomorrow today to replace the production of today.

There are only really four routes available to oil-producing states and major companies which find themselves in this position:

1) invest massively in hydrocarbon exploration, on a scale to challenge conventional perceptions of likely success rates and commercial benefits;

2) invest massively in alternative energy technologies and infrastructure and bring them onstream at an unprecedented rate;

3) give up the struggle to increase hydrocarbon production and energy supply, whilst determining to live off fewer barrels, earning higher revenues for now, and storing up problems for the future;

4) acquire another oil-producer, via corporate acquisition or military conquest, using record corporate or state revenues to fund that process.

The differences between these various approaches increasingly serve to define the strategies and policies of some of the world’s largest corporations, and of many of her wealthiest countries, too.

Thanks for educating me more, Roads–I’m aware of escalating prices but not so aware of how it happens. I learned much in this post.

Thank you, Nichole.

We’ve closed our eyes to the developing energy crisis for far too long. I still meet people who tell me blindly that we won’t ever run short of petroleum.

But those people can never explain why we are already running short of it today.

An excellent, insightful piece Roads, and one that should make us all stop and think.

I called a mini-conference at work this morning. My business is affected by oil in two ways; costs and as a source of business through the conference and exhibition industry. Whilst I’m sure the business end will continue to thrive – at least as long as the price rises people will look to spend more to retrieve the Black Gold – the wider question of alternative resources has us all energised.

One of the projects we support is All Energy.

It’s held at the AECC in Aberdeen, May 21 – 22 this year. The event has doubled in size recently and is set for record numbers again this year. Reed Elsevier, owners of Europe’s largest oil & gas conference, is eyeing the show hungrily.

http://www.all-energy.co.uk/

Opinions are divided about the best placed resource to pursue. Nuclear energy is once more in vogue, but as long as we insist on burying our radioactive waste in the Earth like demented cats we can’t really push this can we? Some interesting – and wacky – suggestions came out of our discussion today. How about firing nuclear waste at the Sun? It is, after all, a giant reactor. Some wag pointed out that you’d need to burn an awful lot of fuel to launch the iradiated waste but I maintain solar sails are the answer to that.

Wind, wave, solar . . . all these energies have potential, but can we harness them efficiently enough to feed our greed for power? What of the NIMBYs who deride any attempt to alter our landscape? Can we afford the time to fiddle while Rome – heck, the whole darned Planet – burns?

Once again Roads you’ve stoked the fires of debate. Good man.

Thanks, Sweder. Firing nuclear waste at the sun is straight out of Solaris, or even Armageddon. I can imagine Bruce Willis or George Clooney at the controls, alongside demented geeks and wild Texan drillers.

But imagine the fallout (literally) if there were a space shuttle disaster releasing the material right across the atmosphere. The wide dispersal of radionuclides was bad enough coming from a ground source at Chernobyl.

What about alternatives? Good question. Offshore wind power is up to the task around these islands, there are no NIMBY issues, and the technology is working well already. Running costs will be low, but it will take massive investment to build the infrastructure. The plans are essentially already there – we will be accelerating those projects which are now at the planning stage, and adding new capacity in between.

I’ve long wondered if you’re a petroleum geologist.

Oil…the cause of so much progress…and so much suffering. I hope we develop alternatives, and fast, for a myriad of reasons.

By the by, given China’s land mass, why is it that China cannot claim vast oil reserves? Just curious.

Aye, that I am, Captain. The proverbial pot calling the kettle black.

Guilty as charged – whilst trying to use my education and insights to change the world, just one word at a time.

China does have some oil, in the South China Sea, but not much onshore. The restricted marine mudstones which form the source rock of most oil deposits were either not developed on China’s landmass, were eroded, or were overcooked by deep burial and mountain building.

Extremely worrying, though, is that China has massive and abundant resources of coal, and she is presently commissioning five new coal-fired power stations each and every week. If China continues to follow this route (and in the absence of a compromise from the US on Kyoto, it is surely inevitable that she will) then the current rates of atmospheric CO2 rise will look positively benign within just a few years from now.

Oh, I do so admire that heart and mind of yours, Roads. No need to feel any guilt. Without you, I’d be out of work (I’ve spent the last three decades cleaning up hazardous wastes…I’ve seen a lot of oil fields).

I’m still wondering about China, though.

Oops, I think I got caught in that old “time-warp” again. You’ve answered my question before it even appeared on your blog.

Then again…I’ve always been lost in time-warp continuum.

Carry on.

Thanks, Jonas. I was just going back to add some more thoughts when you posted. And even then, I’m still wondering about China, too.

Yes, China . . . we talked about China.

China and India; emerging markets with rocketing energy demands, hardly likely to heed our enironmental bleating as they strive to keep up with the Joneses.

Good point about potential striken-shuttle intra-atmosphere fall-out. I’m sure our scientists can produce a fail-safe capsule to hold the waste; they’ll probably name them Titan Intergalactic Containers – or TitanIC for short.

Solar powered vehicles are a real prospect.

I holidayed in France last year (near Gemozac, East of la Gironde, travel by ferry and car, marginally better than flying) where I met a fabulously mad inventor. He’d built the Gites in which we stayed, but his passion is/ was solar transport. He designed a prototype ‘local transport vehicle’ (buggy to you and me) powered entirely by the sun; it can haul a small house and has a top speed of 45 kph. He’s talking to the Bordeaux government about providing a range for seafront and in-town transportation. He was weary when we spoke, tired of failed projects and nervous backers, but he convinced me that solar power combined with gel battery storage can work now on a limited scale.

http://www.maisonborges.com/mborges.html

(scroll to the bottom of the page to see pictures of two of the buggies)

He’d designed a range of off-road vehicles – to service golf courses (including buggies), leisure parks, theme parks and the like. This technology can be extrapolated to serve inner cities and towns – people carriers, personal transports, small package haulage – limiting petrol or hybrid powered vehicles to inter-city tollways.

I’ve no technical expertise but what he showed me made perfect sense. The solar panels drip-charge (even in overcast conditions), feeding the gel batteries. The model he showed me was over ten years old, in constant use (traveling an average of 10 kms every day), hadn’t been refurbed (original battery) and was in perfect working order. He had inter-changeable parts to convert for different uses – pulling a carriage, carrying bulk loads, operating on rough terrain – it was like a giant, lightweight Meccano set.

The only downside I could see was the darned thing was entirely silent. Perfect for preserving the peace, perilous for pedestrians! But if one old buffer from Lancashire can come up with something only one step and a few hundred thousand euros away from production, think what we might achieve with concerted, collective will.

It can be done; we need the political courage to go with the determination.

The BBC News tonight featured a French prototype car which runs on compressed air stored in carbon fibre tanks. It boasts a top speed of 80mph and a list price of just £2,500 ($5,000).

Meanwhile, the Mayor of London, ‘Red’ Ken Livingstone today announced that he is tripling the Daily Congestion Charge for SUVs entering Central London to £25 ($50). I can hear the billionaire bankers of Kensington and Chelsea bleating over their Bollinger already.

I must admit that I was very sceptical about Livingstone at one time. Like all great politicians, he lives near to the edge on occasion.

Telling that (Jewish) journalist he would have been a disgrace to the Nazi Party was bluntly insensitive, even for Ken, and even if it showed a refreshingly honest assessment of the editorial policy in the Daily Express.

But for all of his occasional failings, Livingstone has really got some great things done.

Looking back, it’s clear he would have made a brilliant Prime Minister, if only we could have ever remotely considered electing him. On green issues, Ken has been simply outstanding. Let’s nominate him for a Nobel Peace Prize, under the slogan: Al Gore speaks about change, and Ken Livingstone acts to accomplish it.

Well, well. Energy. The big bugaboo.

No simple solutions to be sure. Massive paradigm shift seems likely….William Calvin, a neurobiologist/brain author, has suggested that the human brain was fully developed to its current ‘size’ long before we actually started using it … he suggests that a ‘environmental catastrophe’ sparked the first ‘big bang’ in human consciousness. In simple terms, as a species, we MUST adapt, (and stop fouling our own nest), or we die…. Could be we are now at the second ‘big bang’ ‘threshold’ , sooooooo, keep this tickers tinkin’ ! We may have hit ‘peak’ oil production, but we are no where near the ‘critical mass’ of what human beings can and SHOULD do.

Also, complete aside, it’s my understanding that Barack Obama’s delinquent absentee dad was a ‘Kenyan economist’ of some kind … know anything about that or who that might be? Does he have any kind of profile in Kenya today? Just idle internet roaming curiosity… as per usual … Best, C

Yes, canadada – I agree that we are capable of finding good energy solutions. We just need the brains to start implementing them.

Barack Obama’s father? Let me ask that question over at From Scratch. Ella is a fan, and she’s in the know on all the background, too.

I’m so sorry I missed the question in my inbox. In any case, I’ve answered on canadada’s blog but here’s what I know for anyone else who’s interested:

Obama’s parents are dead. His father was Barack Obama, Sr (many don’t realize Barry’s a Jr) and after abandoning his family, and possibly after a stop at Harvard (conflicting info there) he did in fact return to his homeland. I’ve seen him described as a “bureaucrat” there but don’t know what that means.

One of Obama’s grandmothers is still alive and I seem to think she lives in Hawaii, as his half-sister certainly does. Hawaii’s primary is Tuesday and he will, of course, have the native son advantage.

Barry!

Thanks, Ella. The campaign is at a fascinating, and possibly decisive stage.

The newspaper reports I’m reading here this weekend seem to suggest that Obama’s momentum is continuing to grow, and that Hillary’s team is beginning to struggle for finance.

Can Obama convert this shift in popular mood into electoral success through Texas and Ohio? It’s going to be compelling to watch.

Interestingly, the BBC seems to have hardly had anything to say on your elections since quite early on in the Super Tuesday declarations, apparently leaving Hillary still in a significant lead. And I’m not quite sure why that is.

They did carry a Matt Frei interview with George Bush last week, though. It was astonishing to see the President steadfastly defending the practice of waterboarding as a useful contribution to justice.

Amongst the many options open to him now, including writing it off as some kind of grotesque mistake, or even as a regrettable experiment, the choice of full-blooded support didn’t look such a wise move at this distance.

It’s coverage like this which goes a long way towards explaining a growing determination to select a different kind of candidate this time. Surely there’s a real opportunity now for a leap into a different kind of future.

Barry definitely has momentum (the ‘big mo’ as they say inside the Beltway) and even though Hillary loaned her campaign $5 million a few weeks ago, I wouldn’t say she’s in trouble financially. Her campaign just spends like crazy. Case in point: She had countless signs here, about 6 feet long and 4 feet tall that say New Hampshire for Hillary. All that money for signs that could never be used in any other state. I don’t know if they were all distributed but if not, they’re all destined for the trash if she’s not the nominee. She has also cut new ads for Texas in Spanish. Not cheap to produce or buy the time.

I’m surprised by the Beeb; editorializing by omission is as potent as the Murdoch style, although I’m not saying BBC is editorializing. (Perhaps Katy Kay is spending too much time prepping for her appearances on Chris Matthews’ talk shows….)

It may just be that the BBC is locked up in its comprehensive coverage of the forthcoming domestic economic meltdown. The Northern Rock bank was finally nationalised yesterday.

The business reporters have all become stars within the past few months. And I suspect that we’ll be seeing a lot more of them as the year unfolds…

Pingback: links for 2008-02-22 « mghicks

The comments on the reddit of this post are quite educational in showing what people think they know about oil supply.

Petroleum is a massively cyclical and risky business, which requires billions of dollars and lots of time to bring new resources onstream. It’s technical risk multiplied by financial risk multiplied by the sheer time-cost of huge amounts of investment money which define that equation.

Post credit-crunch it’s very hard for smaller companies to raise investment cash to fund new exploration projects. Meanwhile, the majors are producing record revenues and profits from declining production, much of which comes from historical giant discoveries made many years ago.

Why invest (and risk) that money for uncertain returns in non-material projects offered by smaller, more complex fields? In consequence, past production growth targets are progressively being abandoned.

Strangely, then, the higher oil price seems to have made the investment fundamentals here shift towards a more risk-averse approach to exploration. That’s because currently it’s a profitable alternative to sit back and just keep pumping, even at a slower rate.

Oil price hits fresh record above $109.

Oil rise sees price touch $111.

Oil price touches new high of $111.80

I’ve tried to imagine scenarios in which the price of oil goes down significantly and I can’t.

One reason for doing so, just as a thought experiment, is to rehearse Pierre Wack’s brilliant analysis which saved Shell a fortune in the 80s when it correctly predicted the price would go down at a time when there was a scramble for reserves.

(During which, incidentally, US Steel gobbled up Marathon Oil–in whose former London office I now live).

Former colleagues at Petroconsultants used to plot peaks of every conceivable kind every day when I worked there (you’ll have seen this http://www.planetforlife.com/htmlfiles/End%20of%20Cheap%20Oil.htm and more) but I haven’t thought much about it lately. I’ve read that $40 of the current price is speculation. I’ve no idea how exaggerated that is.

I think a recession in the US or globally, or a technology breakthrough, likely and very unlikely I suspect, respectively, might help. Meanwhile, I have more or less given up using a car, for now.

Thank you, Paul, and I share your view. Perhaps 30-40% of the current oil price might be attributable to speculation, particularly with oil seen as a hedge against the falling value of the dollar. We might expect some of that to unwind in coming months.

A question remains about how much a recession ahead will decrease global demand for oil. Not that much, I suspect. This means that as world petroleum supply gradually enters a downward curve, oil prices are likely to continue their relentless rise within the medium to longer term.

Falling stocks push oil to $112.

Brent crude at record high close.

Oil price hits $113.93 a barrel.

Oil hovers near $115 record high…

… and I’ve a feeling that $100 oil might soon be a fond and distant memory.

Oil reaches $117 for first time.

Oil rises to yet another record: $117.76.

Oil pauses for breath near $120.

The Independent – Hamish McRae:

A permanently high oil price might not be a bad thing if it forces conservation.

The Independent – Hamish McRae:

Why we will never have cheap oil again.

Opec warns oil could reach $200

Price of oil passes $122.

And what is The Economist saying now?

In one respect, it is different now, at least in the States. Our roads are clogged with gas-guzzling SUVs that didn’t exist then.

Goldman Sachs:

Oil price may hit $200 a barrel – within six months

It’s interesting that analysts are always good at predicting a continuation of an established market trend. They’re much less good at predicting a change in sentiment.

Seeing the analysts now belatedly jumping on the bandwagon in predicting a continued steady rise in oil prices could be taken as one of the clearest signals that the current bull run must be almost over.

At least for now – and perhaps a downward correction looks increasingly likely. But not for long – the fundamentals seem increasingly robust, and there is little evidence of consumers being capable of reducing consumption, even if they were really minded to do so.

It’ll take a good while to replace that fleet of SUVs with more fuel-efficient vehicles. And sadly I suspect that basic domestic economics will finally complete the task much more efficiently than any amount of common sense or altruistic ecologically-minded thinking.

In the meantime we now have a backlash in progress, remarkable for the establishment support of irresponsible planet-trashers in their unexpected hour of need. In America, Hillary Clinton is proposing a ‘gas sales tax holiday’ to assist poor dumb motorists who bought huge cars that were simply too expensive to run.

Over here, new London mayor Boris Johnson is planning in his mindlessly populist way to scrap increased congestion charges for SUVs driven in the city centre by misguided folks who sadly confused the Clapham rush-hour with the Congolese jungle.

Perhaps this all just goes to show how little appreciation we have of the easy availability of cheap fuel. The process of finding, extracting and supplying petroleum has been taken for granted for decades. And that is something which is going to change quite quickly in the months and years ahead.

Perhaps this all just goes to show how little appreciation we have of the easy availability of cheap fuel.

I think that’s key. Here, cheap fuel seems to be regarded as a birthright and if the current situation doesn’t cause a shift in fundamental beliefs, nothing will. I fear nothing will.

Hillary Clinton’s piggybacking onto John McCain’s fuel tax holiday is an abomination. The very idea is ridiculous, but her willingness to pander, even if it means aligning herself with an opponent she desipises, says more about her than him or the situation. Hillary, go away, by whatever vehicle you choose. Hummer, SUV, a reasonable compact car or on horseback .. just go.

I recommend to all your readers interested in this topic the Hamish McRae piece linked to above.

Supply worries push oil near $124

New oil price record high: $124.70

Chronicles Of Depression 2.0: #090

Chronicles Of Depression 2.0: #091

It looks like $200/barrel by 2009.

We just hit $100 earlier this year and it’s already up another 25%!

Pingback: Chronicles Of Depression 2.0: #092 « Mike Cane 2008

Another record as oil passes $126

Get used to it — sky-high oil prices are here to stay.

Oil prices edge towards $128 per barrel

Oil tops $132 for first time

Oil peaks above $135

Oil may reach $150 by July 4th: Morgan Stanley

Oil Prices Take a Nerve-Rattling Jump Past $138

Oil hike sparks ‘serious concern’

Crude oil price rises more than $10 to another record;

Gasoline prices reach an all-time record

Gazprom predicts $250 oil in 2009

Oil rises on crude supply concern

BP says supply/demand driving oil price, not speculation

Why the oil price is high

– by Paul Craig Roberts

Oil at record near $140 a barrel

Oil price bursts through $142

Oil breaks new ground above $143

Oil marches towards $150 a barrel

Opec head sees new oil price rise

London oil price hits $146 record

Oil hits $147 on Iran fears

Higher oil prices lead to fewer drivers – almost ten billion fewer miles driven in May

Oil ‘could hit $200’.

Oil price falls on lower demand.

Oil falls amid economic concerns.

With a financial crash now well under way, and the prospect of full-blown recession looming all around the world, the oil price is in freefall this week at around $90 – a figure not seen since January 2008.

As speculation unwinds, forward trends will be increasingly driven by the downward direction of the market, as short selling of oil futures increases.

Whilst US oil consumption is now falling in response to higher prices, global energy usage has continued to rise modestly, at least until recently (see previous links). The fundamentals of oil supply remain largely unchanged.

Nevertheless, it’s quite likely that the market will now over-correct as the oil price falls from its July peak of $147. But by how much? In this situation, it’s hard to predict the floor. It always is, as the market tends to swing from one extreme of sentiment to another.

Supply and demand, overprinted by wildly fluctuating confidence and speculation. It’s a complex combination. But the bottom line is that none of this uncertainty has created any more oil reserves than there were last week. And falling prices likely mean that we will once more use those reserves at a faster rate.

For now, my bet is that petrol will be cheaper again next week, and for a few more weeks to come. And in an ecological sense, that’s not good news for the future of the environment on this planet.

Matt Simmons: Here comes $500 oil

Concern over US economy rescue package fuels new oil price surge:

Oil price climbs $16 in a single day

My comment last week predicted an increase in the short-selling of oil as the market bubble unwinds.

Following moves to ban short-selling of shares in London and New York, commodity speculation may now gather increased momentum.

Yesterday saw the end of the October oil futures market, and the technical correction was spectacular and aberrant. The oil price fluctuated across a range of over $25 in a single session, before closing $16 up on the day.

This morning’s trend is sharply down again, as traders bank profits. The implication is that we can expect continued instability in oil prices unless or until this kind of speculation is also brought under control.

Uncertainty like this is not good for business planning.

Plot thickens over oil in boom and bust saga

Oil price down to $66 – Brown calls for cheaper petrol

OPEC calls emergency summit as oil price halves

Oil back above $74 as OPEC eyes two cuts

Oil falls to $64, OPEC cuts production by 1.5 mm bopd

Oil falls to $63 despite production cuts

Brent falls below $60

Oil plunges 5% on economic news:

West Texas $59, Brent $55

Oil prices slide another 5%, to 22-month low:

West Texas $56, Brent $52

Oil price steadies below $50

US jobs figures push Brent oil below $40

Merrill Lynch: oil could fall below $25

Goldman Sachs forecasts $45 oil price through 2009 — global shares plummet after US auto bailout fails

Oil dips below $35

Rising inventories and faltering demand drive crude prices lower.

Oil price up to $45 on lower inventories, rising petrol demand.

Is this the bottom of the cycle, or just a dead-cat bounce? The analysts see no rise in sight. Which often means…

Oil trades around $54 on stock market rally

That’s up $20 in five weeks — around a 60% rise since mid-February 2009.

Fascinating read from start to finish.

In your estimation, is there enough production capability to feed the current lowered demand for oil worldwide in this recession?

I read how stocks of oil – in the US for example -have built up, which lowers the price, but I have no idea how long those stocks would last in a not-so-dramatic upturn in world economies.

Do you know how long those oil stocks would last – Are we talking in terms of days, weeks, or months?

Thank you, David. I’m glad you enjoyed this article. A lot has happened since I wrote it in February 2008 — oil prices continued to rise through that summer (peaking at $147 in July 2008) before slumping towards $40 by year end and hitting $34 in January and February 2009. Oil prices have subsequently risen to just over $50 as of 21 April 2009.

The record high oil prices set last summer were followed in the autumn by the most rapid decline in energy prices that the world has ever seen. It has been a rollercoaster ride, exacerbated by the economic crisis of late 2008.

The oil stocks referred to in the press are short-term tank inventories, typically of 90 to 360 day capacity. These are distinct from the discovered but as yet unproduced pools of oil (reserves) which remain buried in the ground for future extraction. Current estimates see over 30 years of oil reserves remaining, but production rates will likely soon fall below world demand. See the first part of Running low on fuel for details.

To answer the first part of your question, there is presently enough production capability to feed the current lowered global demand, with some limited capacity to spare. Nevertheless, the scope for oversupply is not high — and together with recent OPEC production cuts this has placed a floor under the oil price at around $40.

Much of the short-term variation over the past year or so has reflected the effects of speculation. It’s worth bearing in mind that typically around three times as much oil is traded each day as the world consumes, and even this historical multiple may well have been exceeded within recent times.

Thus when prices were rising, traders built long positions, and continued to buy as they bet on this trend continuing. As soon as an identifiable peak was reached, that situation flipped, and traders shorted oil. Some serious anomalies built up as monthly futures contracts expired during the autumn — in the comments stream above I note an occasion when the forward oil price fluctuated by more than $25 on one day alone.

The weekly ebb and flow of economic sentiment often has an impact on the oil price. For example fears about the future of US car manufacturers this spring served to downgrade the market’s view of future oil demand.

One key piece of economic data is the change in oil inventories from month to month. The 26 member states of the International Energy Agency each hold a minimum 90 day strategic reserve, and many have the capability of storing much more — in the case of the US, up to a year’s supply might theoretically be stockpiled if all the tanks were full.

Two different oil prices are widely quoted on world markets — West Texas Intermediate (US Gulf of Mexico) and Brent (UK North Sea). Historically Brent has traded at a $2-3 discount to WTI, reflecting higher transport costs to the centres of demand, but a reversal of that differential in early 2009 told of limited spare storage capacity in the US at that time.

Thus the drawdown or build-up of oil inventories provides evidence of global and national demand in a tangible way that forecasts can not match. Nevertheless, inventory data are prone to later adjustment and are highly seasonal — inventories are built before each Northern Hemisphere winter and gasoline is stockpiled ahead of the US ‘driving season’ in early summer.

All other things being equal (which, of course, they never are) then states would try to build inventories during times of low oil price, and be happy to use those cheaper stocks during price peaks. Anyone who has ever tried to optimise the purchase of a tank of domestic heating oil before the winter will appreciate just how hard it is to get that right. If the price is rising then the temptation is to buy, and if it is falling then you will attempt to wait — forcing the price still higher or depressing it further in each case.

Although a severe world depression would likely have a significant impact on petroleum demand, it’s easy for us (and for the market) to overplay the effects of recession on energy consumption — even within a marked and prolonged downturn like the one we see today.

The US Energy Information Agency compiles an interesting dataset on the US and global petroleum supply balance. In Q4 2008, US petroleum demand was 19.28 mm bbl per day, representing a decline of around 6.3% on a year earlier. In the same period, global petroleum demand fell from 87.00 to 85.74 mm bbl — a decline of just under 1.5%. The effects of the US economic downturn may still be unwinding around the globe, and we may see these numbers converging in 2009 as the US begins to move towards recovery and the world economy continues to slow.

However, even if global petroleum demand falls by 5% from its 2007 peak by this year end, that will merely bring us back to the levels of consumption in 2004. And it’s absolutely critical to recognise that the economic downturn has not in itself created any more petroleum.

The converse is much more likely true — since the collapse in energy prices through late 2008 and the closure of the capital markets since then have resulted in a dramatic reduction in the exploration effort to replace the energy reserves which we persist in using up at a phenomenal rate. And no matter how severe the economic news continues to appear, there still are cars driving up and down the street outside my window as I write.

We’re continuing to deplete the finite energy reserves we have available to us, and so in the longer term upward pressure on oil prices must resume.

I hope that helps to answer your questions, and thanks again for asking.

Great explanation.

One question, where you say “It’s worth bearing in mind that typically around three times as much oil is traded each day as the world consumes..” how does this work? I mean, if a trawler catches fish it is sold on the dock to the wholesaler and then to the shop and then to the consumer, so that is the same fish being traded three times – but I assume you mean on the secondary market with people just trading the assets as middlemen to get some value out of the trade but without ever handling them. How does that work?

Thanks, David, and yes, your second answer is closer to the mark.

The reason that several times as much oil is traded as consumed is that only a fraction of the trades carried out are by people and organisations who intend to use or hold the oil. Many more trades take place between organisations and people who are simply trading to make money — as is the case with other commodities, currencies, bonds and equities.

Just as on the stock exchange, whilst many will stand to benefit from a rise in the oil price, some players will take ‘short’ positions where they hope to make money from a fall in price. This is the way that modern markets work, and looked at from a distance it’s why the movement of the market seems to be affected more and more by its direction than by the fundamentals.